What Are the General Eligibility Requirements?

To get a personal loan in Singapore, you need to meet a few basic rules. These help lenders see if you can repay the loan without problems. While banks and moneylenders may have different terms, the key requirements are similar.

General Guidelines:

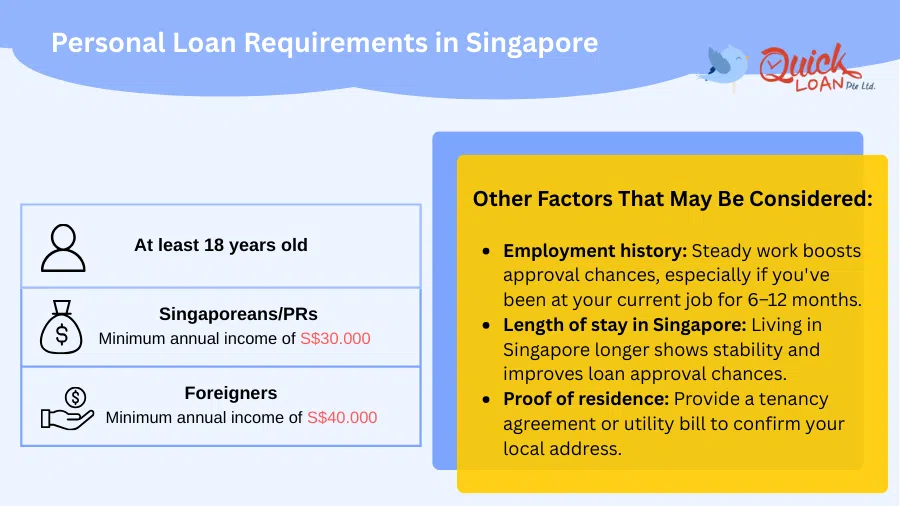

- Age: You must be at least 18 years old to borrow from licensed moneylenders. For banks, the minimum age is 21 years old.

- Residency: You must be a Singaporean, Permanent Resident (PR), or a foreigner with a valid work pass like an Employment Pass (EP) or S Pass.

- Employment: Being employed or self-employed helps. If you’ve worked at your job for at least 6 to 12 months, your chances of getting approved are higher.

- Income: For moneylenders, the minimum income is $10,000 a year. Banks usually require between $20,000 to $30,000 a year or more.

What Documents Are Required for Personal Loans in Singapore

Before you apply for a personal loan, it’s important to have the right documents ready. This helps speed up the process and increases your chances of getting approved.

Lenders need to check who you are, how much you earn, and where you live. Depending on your job type and residency status, the documents may differ slightly.

1. For Employees:

If you’re working for a company, these documents show that you have a regular job and a steady income. Here’s what you’ll usually need:

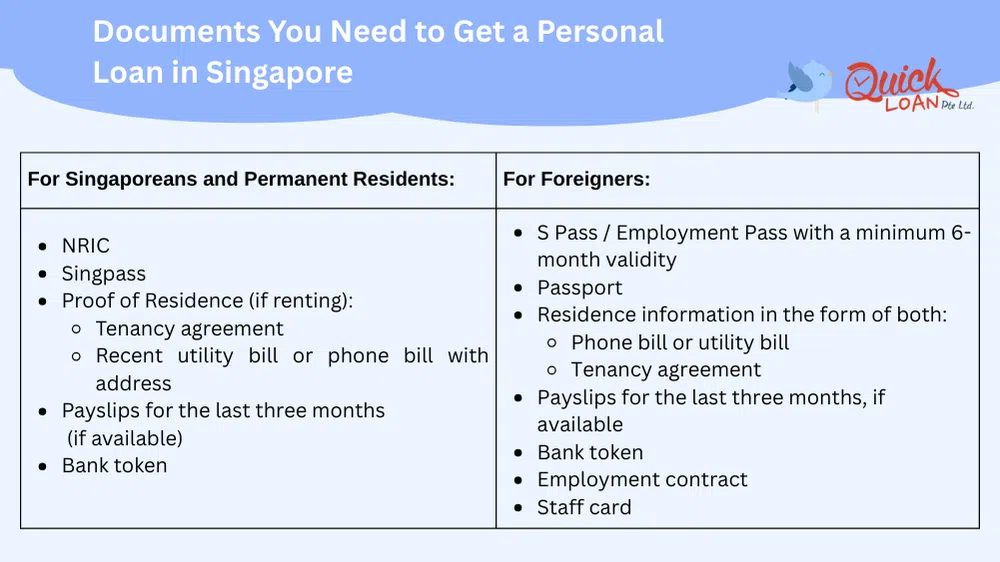

- Identification:

- Singaporeans and PRs: NRIC (front and back)

- Foreigners: Passport and valid work pass (e.g., Employment Pass or S Pass)

- Singaporeans and PRs: NRIC (front and back)

- Proof of Income:

- Recent payslips (last 3 months)

- CPF contribution statements

- Recent payslips (last 3 months)

2. For Self-Employed Individuals

If you work for yourself or run a business, lenders may need extra details. This is because self-employed income can vary. Lenders may use your tax records and bank history to check how stable your income is:

- Identification:

- Same as above – NRIC for locals, passport and work pass for foreigners

- Same as above – NRIC for locals, passport and work pass for foreigners

- Proof of Income:

- Your latest Income Tax Notice of Assessment (NOA)

- Bank statements showing income deposits (usually over the last 3 to 6 months)

- Your latest Income Tax Notice of Assessment (NOA)

3. For Foreigners Living in Singapore

Foreigners must provide a few extra documents to show legal status and steady income. Having proper documents as a foreigner will help your application with a lender. This will show that you’re working legally and have a stable living in Singapore.:

- Identification:

- A valid passport

- A valid Employment Pass or S Pass with at least 6 months of validity left

- A valid passport

- Proof of Income:

- Recent payslips (last 3 months)

- A copy of your employment contract

- Recent payslips (last 3 months)

- Proof of Address:

- Tenancy agreement

- Or utility bills showing your name and local address

- Tenancy agreement

Also note that licensed moneylenders like Quick Loan are less stringent than banks. Moneylenders usually need a few basic documents to review your application. They can often give you same-day approval once everything is in place.

What Personal Loan Requirements Does Quick Loan Have?

At Quick Loan, we strive to make the loan application process clear and accessible. We understand that every individual’s situation is unique. As a licensed moneylender, the process is quick, clear, and friendly. This applies to a local or a foreigner working in Singapore.

That’s why we assess each application on a case-by-case basis, ensuring fairness.

To provide clarity, here are the personal loan criteria that we require for borrowers:

- Eligibility:

- Age: At least 18 years old and above.

- Income: As a licensed moneylender, Quick Loan follows the regulations set by the Registry of Moneylenders. This means that your annual income will be a measurement on how much personal loan we can disburse:

- Age: At least 18 years old and above.

| Annual Income | Singaporeans & PRs | Foreigners |

| Below S$10,000 | Up to S$3,000 | Up to S$500 |

| S$10,000 – S$20,000 | Up to S$3,000 | Up to S$3,000 |

| Above S$20,000 | Up to 6x monthly income | Up to 6x monthly income |

- Documents Needed: As outlined in the previous section.

If you’re still asking, “what is a personal loan and how do I apply?” – this guide should give you a clearer picture. To help you understand your personal loan application with Quick Loan, let’s break it down step-by-step:

How to Apply for a Personal Loan with Quick Loan (Step-by-Step)

Step 1: Check If You’re Eligible

Before applying, check that you meet the basic personal loan requirements. Most lenders, including Quick Loan, will need you to:

- Be at least 18 years old

- Have a steady income (salaried, or self-employed such as Grab drivers or Grab delivery are welcome)

- Show a valid NRIC if you’re a Singaporean or PR

- Provide your passport and a valid work pass if you’re a foreigner

Quick Loan also considers people who may not qualify for a bank loan. Every case is looked at carefully and fairly.

Step 2: Prepare Your Documents

Having your documents ready can speed up your application. Most licensed moneylenders only need the basics:

- NRIC (front and back) or passport + work pass

- Proof of income, such as payslips, CPF statements, or bank records

- Proof of address, like a recent utility bill or tenancy agreement

These documents help confirm your identity, income, and where you live.

Step 3: Apply Online For An Appointment

You can apply for a personal loan at Quick Loan online, right from your phone or computer.

After you apply, our customer service team will contact you to set up an appointment.

As required by law, all customers must visit our branch in person to complete the loan process. This step ensures everything is explained clearly and safely.

Step 4: Get Fast Approval

Once you’re at our branch, our team will review your documents. If everything is in order, your loan can be approved within the same visit.

You’ll receive the money on the spot, either in cash or by bank transfer, your choice.

It’s fast, simple, and follows all personal loan requirements under Singapore law.

Step 5: Review and Accept the Loan Offer

Before you confirm the loan, Quick Loan will go through the full details with you:

- Interest rate

- Monthly repayment amount

- Loan period

- Any fees or charges

- Methods of repayment – PayNow / Bank Transfer / Pay cash in store

There are no hidden costs. You’ll know exactly what you’re agreeing to. This makes it easier to plan your payments and stay on track.

Why Are Credit Scores and History Important

Licensed moneylenders check your credit score and history from the Credit Bureau Singapore (CBS) before giving you a personal loan. These reports show how much you’ve borrowed. They also help decide if your loan gets approved.

Essentially, your credit score reflects your financial reliability. Lenders use it to assess the risk of lending to you. A higher credit score boosts your chances of getting a loan. It can also help you qualify for lower interest rates.

Improving your score helps you meet personal loan criteria in Singapore. Here are some easy ways to help boost your credit score:

1. Pay Your Bills on Time

Always pay your loans, credit cards, and phone bills by the due date. Late payments can lower your score and hurt your chances of getting a loan.

2. Keep Your Credit Card Balances Low

Try not to use up your full credit limit. Using only a small part of your card limit shows that you manage your money well.

3. Don’t Apply for Many Loans at Once

Applying for several loans at the same time makes you look risky to lenders. It can lower your score and reduce your chances of getting approved.

If you have multiple loans, consider a consolidation loan. It can help improve your credit score.

Income-Based Loan Limits in Singapore

Licensed moneylenders in Singapore must follow clear rules set by the Registry of Moneylenders. These rules limit how much they can lend based on your income. This helps protect borrowers, especially those with lower income.

Unlike banks, moneylenders may be more flexible. They often help people who don’t meet bank loan criteria. This includes self-employed workers like delivery riders and Grab drivers.

For Singaporeans and Permanent Residents

If you’re a local or PR, here’s a quick look at how much you can borrow:

- Earn less than $10,000 a year: You can borrow up to $3,000

- Earn between $10,000 and $20,000 a year: Still capped at $3,000

- Earn more than $20,000 a year: You may borrow up to 6 times your monthly income

This system helps make sure you don’t fall into too much debt. It also gives you a fair chance to repay comfortably.

Example: If you’re a Singaporean earning $8,000 a month, you can borrow up to $48,000 from a licensed moneylender. That’s 6 × $8,000.

For Foreigners Living in Singapore

Foreigners can also apply, but the limits are a bit stricter. This is because lenders may see them as higher risk. Reasons include shorter stays, job changes, and fewer long-term ties to Singapore.

Here’s how it works for foreigners:

- Earn less than $10,000 a year: You can borrow up to $500

- Earn between $10,000 and $20,000 a year: You can borrow up to $3,000

- Earn more than $20,000 a year: You may borrow up to 6 times your monthly income

Foreigners also need to show more documents. These may include a valid work pass, payslips, employment contract, and tenancy agreement.

What About Banks?

Banks usually have stricter rules than moneylenders. They prefer lending to people who have steady jobs, good credit scores, and stable income. This helps reduce the chance of someone missing repayments. Most banks also ask for a higher annual income before offering a loan.

Banks – Loan Limits (General Guideline)

| Annual Income | How Much You Can Borrow (Banks) |

| Below S$20,000 | Generally not eligible for personal loans* |

| S$20,000 – S$30,000 | Up to 2x your monthly income |

| Above S$30,000 | Up to 4 to 6x your monthly income |

There are exceptions at times:

- Some banks, like DBS, offer personal loans to locals, PRs, or selected foreigners who earn at least $20,000 a year

- Many banks require foreigners to earn $40,000 or above a year to apply

The process is also slower. Banks take more time to review documents and run checks. It can take several days to get approved and receive your funds.

If you can’t meet bank rules or need quick help, try licensed moneylenders like Quick Loan. They are often faster and easier to work with.

They offer same-day approvals and simple requirements. You don’t need a perfect credit score. And they’re more open to all kinds of income. This includes self-employed people like Grab drivers or delivery workers.

Interest Rates and Other Costs in Singapore

When looking into what is a personal loan, it’s good to also understand how interest is charged. In Singapore, lenders use different methods to calculate interest rates. Knowing how each method works helps you make better borrowing choices. This will help you meet the personal loan requirements more confidently.

1. Licensed Moneylenders

- By law, licensed moneylenders can charge a maximum of 4% interest per month, no matter your income.

- This rate is fixed and cannot go higher, even if you are late with a payment.

- For some licensed moneylenders like Quick Loan, interest is only charged on the remaining balance, not the original loan amount. It rewards borrowers who pay on time or early.

Example: If you borrow $5,000 and still owe $2,000, interest is charged on the $2,000 – not the full $5,000.

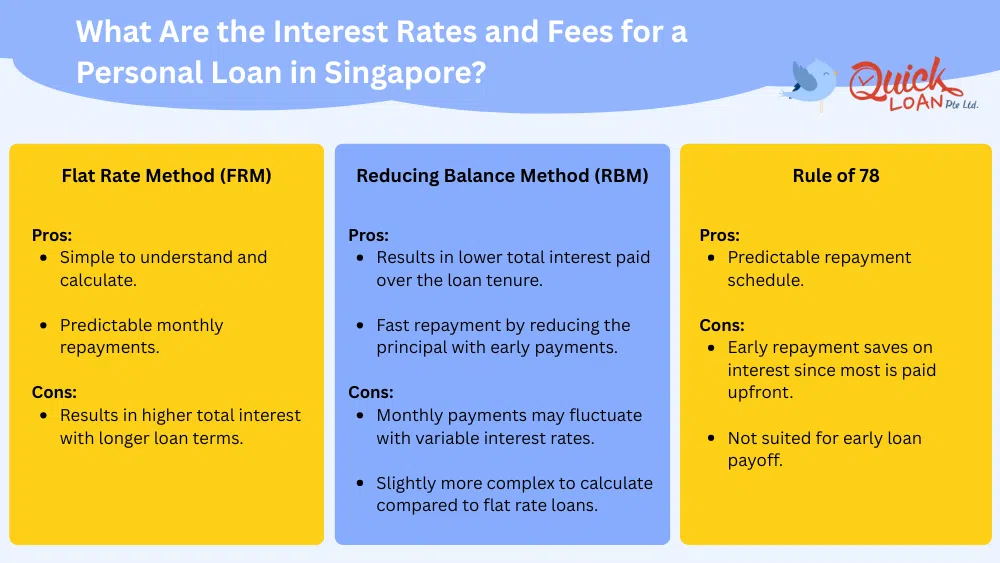

2. Banks

- Banks usually offer a range of interest rates, often ranging from 3% to 7% per year.

- However, banks may have stricter personal loan requirements, such as higher income and a good credit score.

- Some banks may also use different interest calculation methods like the Rule of 78, which makes you pay more interest at the start.

When taking a personal loan, be aware of the associated costs as well. Always read the loan agreement carefully to understand all the costs involved:

- Effective Interest Rate (EIR): This rate shows the nominal interest and extra fees. It gives a clearer picture of the loan’s true cost..

- Processing Fees: One-time fees charged by lenders to process your loan application.

- Late Payment Fees: Charges incurred if you miss a repayment.

- Early Repayment Penalties: Some lenders charge a fee if you repay your loan early.

Tips Before Applying for a Personal Loan in Singapore

Here are some useful quick tips that can help you in applying for a personal loan in Singapore:

1. Compare Different Loan Offers

Compare interest rates, fees, and repayment terms from different lenders. This helps you find a better deal that suits your needs.

2. Check the EIR for Hidden Costs

Always look at the Effective Interest Rate (EIR) – not just the flat rate. The EIR includes all fees and charges. It shows the true cost of the loan. This helps you avoid surprise costs later on.

3. Use Loan Calculators

Loan calculators can show you how much you’ll repay each month and the total cost. It’s a quick way to check if the loan fits your budget.

4. Check Your Credit Report

Your credit report can affect whether your loan gets approved. Make sure all your details are correct. Fix any errors before applying.

5. Avoid Applying for Multiple Loans at the Same Time

Each loan application creates a credit check. Too many at once can hurt your credit score. Choose carefully and apply only when ready.

6. Make Sure You Can Repay On Time

Think about your monthly income and expenses. Only borrow what you’re sure you can repay without stress.

Bottom Line

Understanding personal loan requirements in Singapore is essential especially if you’re planning for bigger financial goals like taking a home loan after a personal loan. Knowing how one loan may affect another can help you plan more confidently. It’s easier to get your loan approved when you’re prepared. Knowing the eligibility criteria, required documents, and costs helps you make smart choices.

This way, you can pick the best personal loan option for your needs. Just remember to borrow only what you really need, and nothing more. This will help your credit score in the long run.

For any questions on what is a personal loan, or personal loan requirements, reach out to Quick Loan. We’ll provide a friendly, no-obligation chat to help you clarify any doubts you might have!