What Is a Personal Loan

A personal loan is money you borrow from a lender. This could be from a bank or licensed moneylender. You can use this loan to pay for a variety of expenses. This includes medical bills, renovations, school fees, weddings, or emergencies.

What makes personal loans unique is that they are usually unsecured. This means you don’t need to give your house, car, or anything else as security to get the loan.

Types of Personal Loan Providers in Singapore

In Singapore, there are mainly two groups you can borrow from:

- Banks and financial institutions usually provide bigger loans and longer repayment terms. Borrowers, however, must have a good credit score. They also need a stable income and higher minimum income levels.

- Licensed moneylenders are approved by the Registry of Moneylenders. They have more lenient requirements compared to banks and are open to a wider range of borrowers, including employees, self-employed individuals, and foreigners. They offer fast approvals, flexible terms, and require only basic documentation. Moneylenders are a great option if you are in need of urgent cash.

How Much Can You Borrow from Licensed Moneylenders in Singapore

Licensed moneylenders in Singapore follow strict rules set by the Registry of Moneylenders. These rules are based on your annual income and residency status.Here’s a simple breakdown of how much can a personal loan be:

Licensed Moneylenders – Loan Limits

| Annual Income | Singaporeans & PRs | Foreigners |

| Below S$10,000 | Up to S$3,000 | Up to S$500 |

| S$10,000 – S$20,000 | Up to S$3,000 | Up to S$3,000 |

| Above S$20,000 | Up to 6x monthly income | Up to 6x monthly income |

Maximum Loan Limits for Singapore Citizens and PRs

Licensed moneylenders in Singapore follow strict rules set by the Registry of Moneylenders on how much they can lend.

If you’re a Singaporean or Permanent Resident, here’s how it works:

- Below $10,000 a year: You can borrow up to $3,000.

- Between $10,000 and $20,000 a year: You can borrow up $3,000.

- Above $20,000 a year: You can borrow up to 6 times your monthly income.

This structure helps ensure borrowers do not take on too much debt and are able to repay comfortably.

Maximum Loan Limits for Foreigners

For foreigners working in Singapore, loan limits are slightly stricter:

- Below $10,000 a year: You can borrow up to $500 only.

- Between $10,000 and $20,000: Limit is $3,000.

- Above $20,000: You may borrow up to 6 times your monthly income.

Foreigners are usually asked to provide extra documents. This includes a valid work pass, employment contract, tenancy agreement, and recent payslips.

Unlike banks, licensed moneylenders like Quick Loan offer much faster approvals and simpler loan application processes. Also, they are often more flexible with income types. This makes them a select choice for self-employed or those who require urgent cash.

How Much Personal Loan Can You Borrow from Banks in Singapore

Now let’s talk about banks. The rules aren’t set by law but follow standard banking practices. Banks usually require a higher annual income to lower the risk of non-repayment. They tend to lend only to people with steady jobs, strong credit scores, and reliable income. These qualities ensure banks feel more confident that the loan will be paid back on time.

Here’s what most banks in Singapore offer:

Banks – Loan Limits (General Guideline)

| Annual Income | How Much You Can Borrow (Banks) |

| Below S$20,000 | Generally not eligible for personal loans* |

| S$20,000 – S$30,000 | Up to 2x your monthly income |

| Above S$30,000 | Up to 4 to 6x your monthly income |

*Some banks, like DBS, usually give loans only to Singaporeans, PRs, or certain foreigners who earn at least S$20,000 a year. Otherwise, for foreigners, most banks require a minimum income of $40,000 to $60,000/year to be considered.

For most banks, the application process is often more detailed. This includes stricter requirements and credit checks. As a result, approval and disbursement can take several days – sometimes even longer.

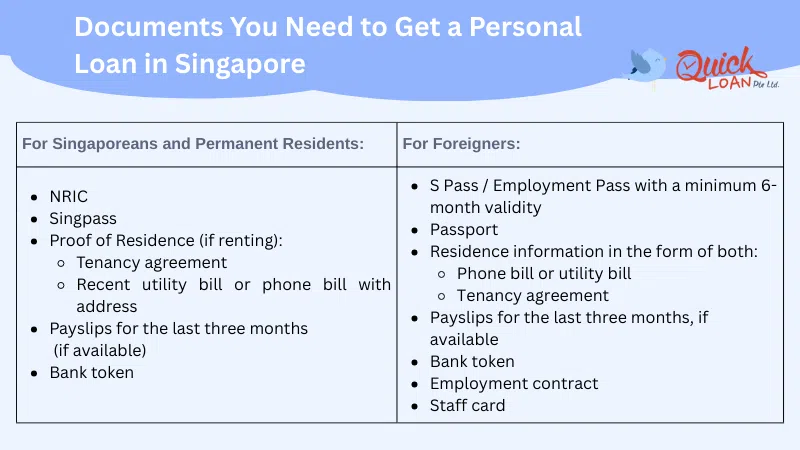

What Do You Need to Qualify for a Personal Loan

To apply with a bank or a licensed moneylender, you must meet basic personal loan requirements. These criteria help lenders decide if you’re able to manage the loan responsibly and repay it on time. Most banks and moneylenders have similar key requirements, even if they vary a bit:

Eligibility Criteria (General Guidelines)

- Minimum age: You must be at least 18 years old to apply for a personal loan at most licensed moneylenders. However, banks have a higher minimum age limit at 21 years old.

- Residency: You must be a Singaporean, Permanent Resident (PR), or valid work pass holder. A valid Employment Pass (EP) or S Pass usually falls under the last category.

- Employment: Being under a salaried, self-employed, or freelancer employment helps. If you’ve worked in your current position for 6 to 12 months, your chances of getting a loan approved are better.

- Income: Minimum annual income usually starts at $10,000 for moneylenders; $20,000–$30,000 for banks.

On top of this, there are other common documents that will be necessary for your application.

Common Documents Needed

- NRIC (or Passport + Work Pass)

- Recent Payslips

- Income Tax Notice of Assessment (for self-employed)

- Proof of Address (utility bill, tenancy agreement)

- Employment contract (especially for foreigners)

Borrowers seeking personal loans from banks usually need extra documents, besides the ones listed. This can include your latest Income Tax Notice of Assessment (NOA) or CPF Contribution Statements.

Licensed moneylenders like Quick Loan often need just a few basic documents to review your application.

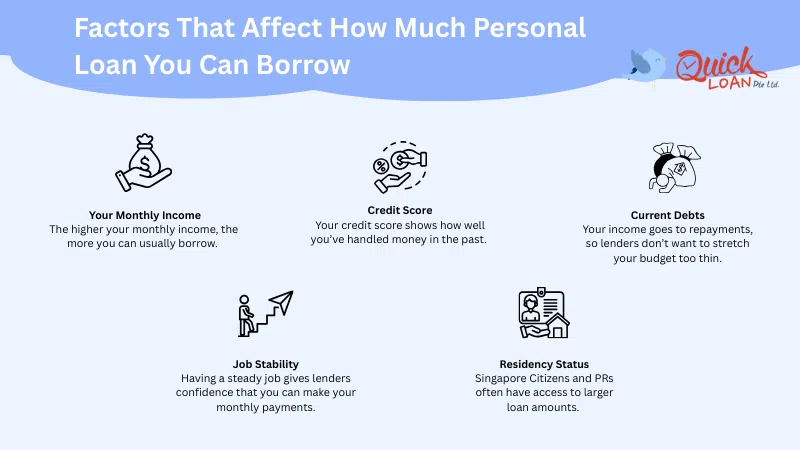

Factors That Affect How Much You Can Borrow on a Personal Loan

Even if you’re eligible for a personal loan, the actual amount you can borrow isn’t guaranteed. Lenders still need to look at a few key things to decide how much they’re comfortable lending you. These checks help make sure you can manage the repayments without trouble:

1. Your Monthly Income

The higher your monthly income, the more you can usually borrow. Lenders look at your income to decide how much you can pay back. Licensed moneylenders may allow you to borrow up to 6 times your monthly income if you qualify.

2. Credit Score

Your credit score shows how well you’ve handled money in the past. Lenders become cautious if you miss bill payments, max out credit cards, or have past loan issues. A good score can help you get a higher loan amount and better terms.

3. Current Debts

Already paying off a car loan, credit card, or another personal loan? Lenders may reduce your borrowing limit to avoid overloading your monthly budget. Your income goes to repayments, so they don’t want to stretch your budget too thin.

4. Job Stability

Having a steady job gives lenders confidence that you can make your monthly payments. Banks prefer full-time workers, but licensed moneylenders accept self-employed, contract, or gig workers.

5. Residency Status

Singapore Citizens and PRs often have access to larger loan amounts. Foreigners might have stricter limits. This is especially true if they’ve been in Singapore for a short time or lack enough paperwork.

Can You Take Multiple Personal Loans in Singapore

Yes, it’s possible to have more than one personal loan but it depends on your situation.

Banks usually prefer giving out just one loan at a time. They might be strict when approving a second loan. This is true, especially if you have other debts.On the other hand, licensed moneylenders like Quick Loan are more flexible. They’ll be happy to look at your case individually. They’re open to giving you another loan if:

- You’ve been a good customer with no late payments

- Your income can support more debt

- The combined loan amount doesn’t exceed your borrowing cap

That said, managing too many loans at once can get confusing. If you already have several repayments, it’s often better to combine your debts into one loan. This way, it’s easier to keep track and avoid missing payments.

What Happens If You Exceed Your Borrowing Limit

Licensed moneylenders in Singapore must follow the rules set by the Registry of Moneylenders. That means they can’t lend you more than what you’re legally allowed to borrow based on your income.

But in some cases, borrowers may take loans from multiple lenders at once. If the total amount you owe goes over the limit, here’s what might happen:

- You may struggle to keep up with the repayments, leading to debt stress

- You could get blacklisted, which affects your chances of getting future loans

- If you miss payments, legal action could be taken against you

Before giving you a loan, most licensed moneylenders always check the Moneylenders Credit Bureau (MLCB). This shows how much you’ve already borrowed and helps them decide whether to approve your loan.

To stay safe, it’s best to borrow only what you truly need – and only from licensed, trustworthy moneylenders like Quick Loan.

How to Increase the Amount You Can Borrow

If you’re hoping to borrow a higher loan amount, there are a few practical things you can do to improve your chances:

1. Improve Your Credit Score

Your credit score shows how well you manage money. Pay your bills on time, avoid missing payments, and try not to max out your credit cards. A better credit score makes lenders more willing to offer you a higher loan.

2. Increase Your Income

The more you earn, the more you can borrow. Try boosting your income by taking on a part-time job, doing freelance work, or asking for a raise. Lenders look at your income to decide what you can afford to repay.

3. Reduce Existing Debts

If you already have other loans or credit card balances, paying them down can help. When you owe less, lenders are more likely to trust that you can handle a new loan comfortably.

4. Apply with a Licensed Moneylender

Licensed moneylenders, like Quick Loan, are often more flexible than banks. They may consider giving you a larger loan, even if your income is irregular or if you’re self-employed. Each case is reviewed individually, so you don’t need a perfect financial record to qualify.

Tip: Always borrow within your means and only take what you really need – not just what you qualify for.

How Much Can You Borrow for a Personal Loan from Quick Loan?

At Quick Loan, how much personal loan you can get depends on two main factors: your annual income and your citizenship status.

Here’s a simple breakdown:

| Your Annual Income | Singaporeans & PRs | Foreigners Living in Singapore |

| Under S$10,000 | Up to S$3,000 | Up to S$500 |

| From S$10,000 to under S$20,000 | Up to S$3,000 | Up to S$3,000 |

| S$20,000 or more | Up to 6× monthly income | Up to 6× monthly income |

Quick Loan does not just look at your credit score. We take time to understand your situation and offer solutions that fit your needs. We also offer support for those who may not qualify at banks, on a case-by-case basis.

Whether you’re a local, PR, or working in Singapore, we’re here to make the process simple, fast, and stress-free.

All you need is to meet these basic requirements:

- At least 18 years old.

- A steady income (we accept salaried employees, self-employed, and foreigners)

- Valid NRIC for locals, or passport + valid work pass for foreigners

- Proof of income, like payslips or bank records

- Proof of address, such as a utility bill or tenancy agreement

If you’re unsure where to begin, here’s a simple guide on how to apply for a personal loan in Singapore.

So, how much can I borrow personal loan in Singapore? The answer depends on many factors – your income, your existing loans, and whether you go to a bank or licensed moneylender.

So, how much personal loan can you get in Singapore? The answer depends on many factors – your income, your existing loans, and whether you go to a bank or licensed moneylender.

Here’s what to remember:

- Licensed moneylenders can lend you up to six times your monthly income. This amount depends on your earnings and residency status.

- Banks may offer more if you earn above $30,000/year, but they have stricter rules.

- Licensed moneylenders like Quick Loan offer fast, fair, and flexible personal loans. They tailor them for your situation.

Borrowing money isn’t a bad thing if it’s done wisely. Only borrow what you need. Read the terms closely. Ensure repayments fit your budget.

If you’re unsure, reach out to Quick Loan for a friendly, no-obligation chat. We’re here to help.